- LRL Financial Newsletter

- Posts

- Case Study: Distressed Office Loan - Part 2

Case Study: Distressed Office Loan - Part 2

This is part 2 of a case study that analyzes the acquisition of an NPL secured by an office building

Edward Bond

March 27, 2025

Welcome back to the LRL Financial Newsletter. Here is the agenda for this week:

Part 2 of the Distressed Office Loan Case Study

A sample of deals in the pipeline

LRL’s bridge lending and NPL acquisition terms

Case Study: Distressed Office Loan - Part 2

If you missed part 1, you can read it here: https://edwards-newsletter-8d1664.beehiiv.com/p/case-study-distressed-office-loan-part-1

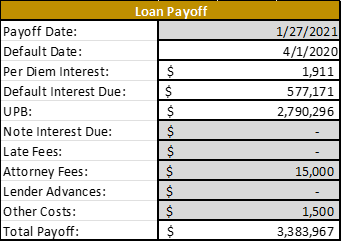

NPL Options and Potential Returns

As we discuss our options, keep in mind the following:

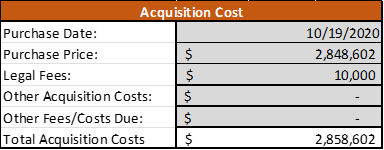

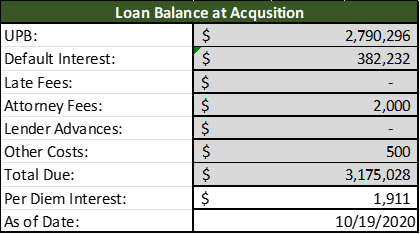

This was discussed in Part 1. Please read it again if you do not remember why the amounts differ.

Option 1: Restructure the loan.

Large credit funds may modify the existing note to establish a repayment history before selling it. Typically, they buy large pools of NPLs, attempt to restructure the loan by changing the terms (i.e., making the repayment more affordable), and then sell the reperforming loans as a package. Volume and leverage allow the fund to earn sufficient returns. This is a simplistic version of its business plan. We are not a large credit fund, nor have I worked for one in the past decade. Therefore, this is not my area of expertise.

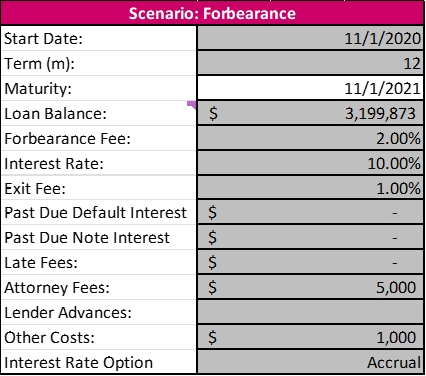

We restructure loans through a forbearance agreement, typically with a short duration of 6 to 18 months. We were prepared to make the following offer to our borrower:

There are a few items to discuss:

We acquired the loan on October 19, 2020. We were prepared to offer a 12-month forbearance agreement.

The loan balance includes the total amount due on October 19th plus 12 days of default interest. The default interest would continue to run until the forbearance agreement was executed. It would then be capitalized. Interest and fees would be charged off this loan balance.

Forbearance Fee

2% of the loan balance

Payable at execution of the forbearance agreement

Interest Rate

10% fixed

This would be our initial offer. Given that the borrower could not make payments at a 4% rate, it was highly unlikely they could at 10%. Therefore, we would have to get creative with our structure.

Instead of making interest payments out of pocket each month, we could allow the 10% to accrue and be due at loan payoff. In return, we could request a minimum amount of interest earned.

For example, we could add a clause that states we are entitled to 6 months of forbearance interest. If the borrower pays off after three months, we will still receive the remaining three months of interest.

If the property has a lot of equity and you know the borrower can either i) sell the property or ii) find a new lender, this can be a good strategy.

Exit Fee

1% of the loan balance

Payable at loan payoff

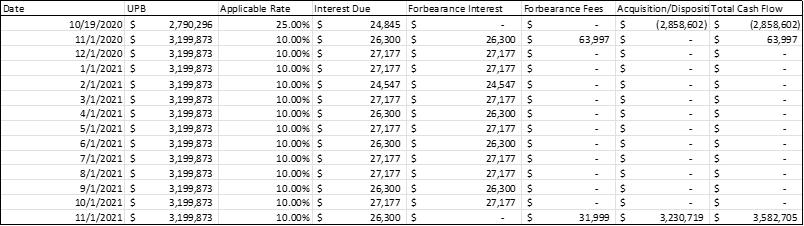

If we accrue the 10% interest for one year, here are the cash flows:

Option 2: Borrower pays off via a property sale or refinance.

As discussed in Part 1, this was the actual result.

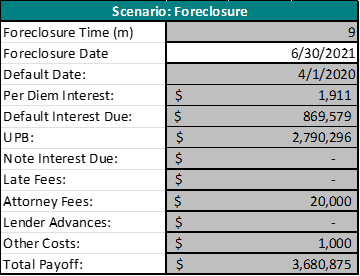

Option 3: Foreclose and take ownership of the collateral.

For simplicity, let’s assume we are paid off at the foreclosure auction. This means an investor bid at the auction and won. If we were to take title to the property, we would start implementing our value-add game plan.

Once again, let’s touch on a few items:

Foreclosure time and date

This is hard to predict. You never know how hard a borrower will fight for the property. They can litigate and delay the foreclosure if they have the financial resources. It is also dependent on the legal jurisdiction.

The borrower could also declare bankruptcy and really slow the process down.

In our jurisdiction, nine months is reasonable, assuming no bankruptcy or crazy litigators.

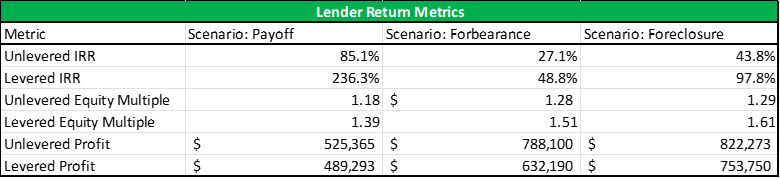

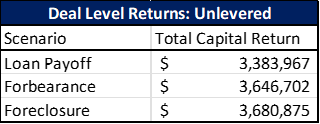

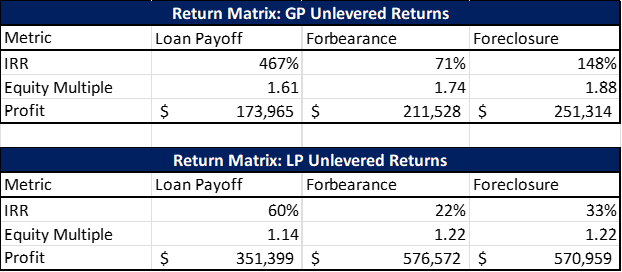

Returns

Based on the above, here are the projected returns under each scenario:

If you are interested in NPL investing, this is a chart you must understand. As mentioned in Part 1, we do not focus on the IRR. When you are paid off quickly, you must find another deal to place that capital, and finding great deals is hard.

Notice the equity multiple and profit across the three scenarios. The Payoff is the lowest. Our capital was only at work for 100 days. The Forbearance could be a good outcome. However, we are accruing interest, and there is no guarantee we will actually be paid off in 12 months. The Foreclosure is a wild card. Between litigation and auction bidders, anything can happen.

We will come back to this chart again. It’s just starting to get interesting.

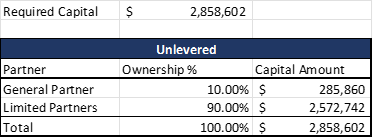

Leverage

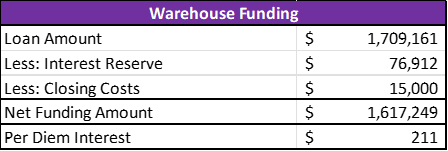

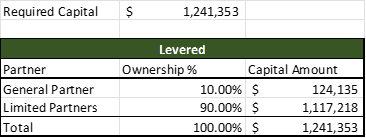

We like to use leverage to (hopefully) amplify our returns. Remember, leverage cuts both ways, so you have to be careful. We utilize a warehouse line to purchase non-performing loans. Put simply, we borrow money from another lender, typically a bank, to fund the note purchases. The lender will fund up to 60% of the note acquisition cost. They charge Prime plus 1% and require 12 months of interest to be held back at closing. Therefore, the lender funded the following at note acquisition:

We were required to fund the balance of $1,241,353. We did not have to worry about paying interest out of pocket for 12 months since it was held back from the loan proceeds. If the loan were still active in a year, we would have been required to fund another 12 months of interest in full.

Note: I will devote an entire post to the mechanics of a warehouse line.

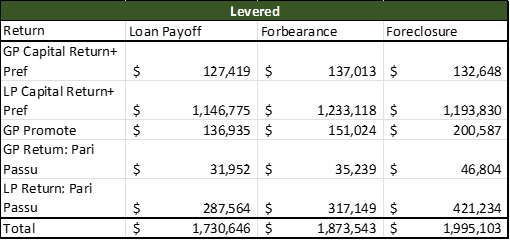

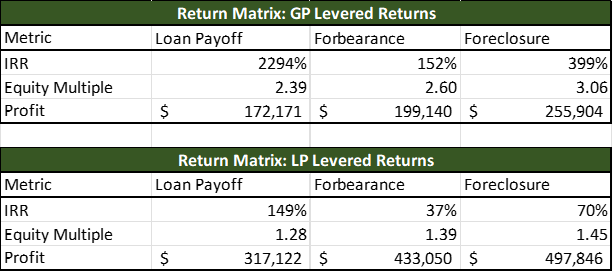

Here are the projected levered and unlevered returns under each scenario:

Although the levered deal profit is lower under each scenario, our IRR and equity multiple improved. This is a function of having less of our cash invested in the deal and leverage being beneficial. The danger of using leverage on an NPL is the unpredictability of exiting the investment. In this deal, leverage was beneficial because we were paid off quickly. However, it could have dragged on for a substantial amount of time. For example,

What if the borrower declared bankruptcy?

What if the borrower had deep pockets and hired a top-tier litigator?

What if we get the property back via foreclosure?

These are just a few questions you must consider when utilizing leverage. All three will result in a longer holding period. As mentioned above, the lender will likely make you replenish the interest reserve in full after it is depleted. You better have the liquidity to replenish it, or you are in default, jeopardizing your entire investment.

This lender offers up to 60% LTC on NPLs. Just because your lender allows 60% leverage doesn’t mean you have to take it. The leverage you utilize should depend on i) the deal and ii) the deal relative to your overall portfolio. We felt comfortable using 60% on this deal due to our legal position, property equity, and overall company liquidity.

Investor Incentives

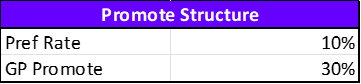

The majority of CRE investors do not own 100% of an investment. It is much more typical to have a General Partner (GP) – Limited Partner (LP) structure. The GP sources the opportunity, contributes a small amount of capital, and then attempts to execute the business plan. The LP contributes most of the capital and monitors the GP’s execution. The return structure incentivizes the GP. The better the investment’s performance, the higher the cash flow allocation to the GP. The fees GPs can generate on deals are another big incentive, but we will save that for a future article.

Let’s revisit the returns for each scenario and analyze how the GP is incentivized to i) pursue a certain outcome and ii) use leverage. Understanding the incentives going into an investment is important, especially as an LP. As you’ll see, a GP can make decisions that disproportionally benefit them but do little for the LP.

The GP will contribute 10% of the capital, and the LP 90%. Remember, we utilize 60% leverage, so the required equity capital is much less under the Levered scenario.

The promote structure is the same for Unlevered and Levered. First, the GP and LP receive their capital back and a 10% return. Second, the GP receives 30% of the excess cash flow (i.e., the promote). Third, the remaining cash flow is split pari passu (pro-rated). This is a clean and easy GP-LP structure.

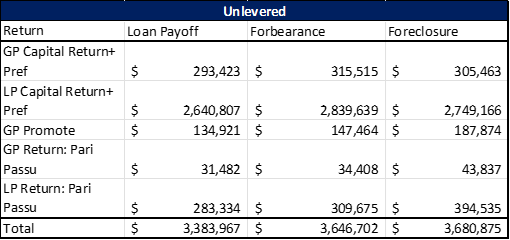

Here is the total capital return under each scenario with and without leverage:

Here is the cash flow allocation per the GP-LP structure:

Finally, the GP and LP returns:

Before you continue reading, stop and think about the outcomes under the three scenarios: loan payoff, forbearance, and foreclosure. Then move on to comparing them with and without leverage. What standouts?

Without a clearly defined investment mandate, the GP can take action that disproportionally benefits them over the LP.

A few observations:

The loan payoff has the highest IRR. This is due to a short holding period. The GP can capture the promote quickly. However, the total deal profit is lower than in the other scenarios. The forbearance and foreclosure scenarios may take longer, but the profit potential is much higher and likely a better outcome for the LP as their capital is invested longer. The GP doesn’t need to take a hammer at every borrower and force a loan payoff. It can be in your investor's best interest to be patient. Allow the default interest to run. Take your time negotiating a forbearance agreement or going through legal proceedings. This isn’t to say you never have to bring out the hammer, but only do so when necessary.

Compare the dollar amount of the GP promote. Under the levered scenario, the required capital contribution is lower, yet the promote is higher. The GP disproportionally benefits from leverage. As an LP, you must negotiate leverage limits with the GP. You have significantly more to lose than the GP.

The higher the GP promote, the more extreme points #1 and #2 can be as more of the benefits flow to the GP. There isn’t a perfect GP-LP structure, but you must consider it when investing in NPLs. The GP may be focused on fees (not discussed here) and realizing the promote as soon as possible. In contrast, the LP is focused on total returns and capital allocation.

LRL Pipeline Deals

Here is a sample of a few deals that should close in the near future:

Deal 1: Our borrower is acquiring an NPL. We are providing note financing at 65% of the note purchase price.

Deal Type | NPL Note Financing |

Collateral | Motel |

Location | Florida |

LTC | 65.00% |

Loan Amount | $2,925,000 |

Interest Rate | 12.00% |

Origination Fee | 2.00% |

Term (m) | 12 |

Minimum Interest (m) | 6 |

Deal 2: Our borrower has to complete a property improvement plan (PIP). We are refinancing the existing loan and providing $1 million for the PIP.

Deal Type | Bridge Loan |

Collateral | Hotel |

Location | New Mexico |

LTV | 65.00% |

Loan Amount | $4,000,000 |

Interest Rate | 12.50% |

Origination Fee | 2.50% |

Term (m) | 12 |

Minimum Interest (m) | 9 |

Deal 3: Our borrower is purchasing a luxury residential property. We are providing short-term financing as this is a quick close.

Deal Type | Bridge Loan |

Collateral | Single Family |

Location | Florida |

LTV | 65.00% |

Loan Amount | $6,500,000 |

Interest Rate | 12.00% |

Origination Fee | 2.00% |

Term (m) | 12 |

Minimum Interest (m) | 9 |

LRL Bridge Loan Terms

Our NPL and note financing criteria are similar. If you have a deal you would like to discuss, please send me an email: [email protected]

Thanks for reading. I’ll continue to add my topics.

Ed