- LRL Financial Newsletter

- Posts

- Case Study: Distressed Office Loan - Part 1

Case Study: Distressed Office Loan - Part 1

This post provides a comprehensive analysis of an nonperforming loan acquisition.

Edward Bond

March 13, 2025

In Q4 2020, a community bank offered to sell a nonperforming loan (NPL) collateralized by an office building. The property’s performance was affected by COVID. While the bank initially deferred loan payments, the borrower failed to resume making payments after the forbearance period expired. We were able to negotiate and close on the loan purchase quickly.

Loan Overview

The bank originated the loan in 2017 with the following terms: a 4% fixed interest rate, a 10-year term, and a 25-year amortization with no interest-only payment period. The original loan amount was $3,000,000, and the appraised value was $5,000,000, equating to a ~60% loan-to-value (LTV). The bank did not require the borrower to escrow property taxes or insurance. Under the loan terms, if the borrower defaulted, the interest rate would increase to the maximum allowed by law. In this case, the state (Florida) permitted a maximum default interest rate of 25%.

The loan had no performance issues (i.e., all payments were on time) until COVID hit in Q1 2020. With the borrower unable to make payments, the bank offered, and the borrower executed, a forbearance agreement in Q2 2020. The bank agreed to forbear loan payments for six months. In return, the interest due during this period would be deferred, and payments would resume in Q4 2020.

Property Overview

The office building was near the County courthouse. It was built in 1975 and totaled approximately 25,000 square feet (SF) across five floors. The entire building consisted of executive office suites, primarily leased to attorneys who had to frequent the courthouse. Most office tenants operated their own law practices and had month-to-month (MTM) leases. When COVID hit, the County moved court hearings to Zoom. Since most of the tenants were MTM, they vacated their suites. Therefore, the property owner (i.e., the borrower) lost a substantial amount of rent and immediately had cash flow issues.

At the time, no one knew when court hearings would resume in person. The existing tenant base had little reason to lease an executive office suite if they did not need access to the courthouse. It was unclear if the borrower could ever generate enough rental income to resume paying the loan again. A forbearance agreement made sense for both sides as there was significant uncertainty in the world due to COVID. Unfortunately, little changed, and the borrower could not resume making payments when the forbearance agreement expired.

Negotiation with Bank

Banks quickly sold nonperforming loans during the Great Financial Crisis (GFC). They offered huge discounts to entice investors to purchase the loans. The banks then witnessed those investors make significant returns over the next few years. This was not lost on management. The ability to negotiate substantial discounts this cycle was much more difficult. From our perspective, there was reason to believe the bank would be open to taking a discount (i.e., less than the outstanding principal).

First, as mentioned in the Loan Overview section, the loan did not require the borrower to escrow property taxes and insurance with the bank. Although the property taxes were not yet delinquent, we had to assume they would be in a few months. Unpaid property taxes result in a lien against the property, and it takes precedence over your mortgage. The bank wants to avoid dealing with or paying for this to protect its collateral. The bank also provided us with insurance certificates showing that the current property and liability coverage ran through March 2021. While this was good news, you must assume they will not have the funds to pay the renewal premium. If the borrower does not pay the insurance premium, the lender better advance it, or the collateral has no protection. The insurance renewal premium would cost another ~$65,000.

Second, if the bank were forced to foreclose and take back the collateral, it would be stuck with a vacant building. While they could bring in a third party to manage and lease the property, someone still has to oversee the process. There are also high costs to re-leasing a building, including leasing commissions, tenant improvement allowances, addressing any deferred maintenance, and carrying costs until the property is cash flow positive. At the end of the day, it is a drain on the bank’s time and resources and out of their core competency.

Finally, the fact that the bank was looking to sell the loan towards the end of the quarter indicated they wanted the loan off their books before the next reporting deadline. While we weren’t privy to their accounting standards and processes, they would likely have to write down the loan in some capacity (i.e., it would impact their bottom line).

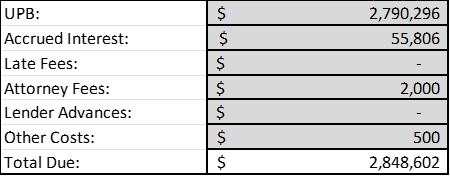

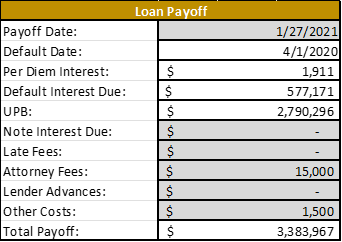

Most banks understand these points, but we like to remind them when presenting an offer. We eventually agreed to purchase the loan for the total outstanding balance. As of the loan closing, the borrower owed the following:

As noted in the Loan Overview section, the interest rate would increase to 25% if the borrower defaulted. Due to the client relationship, banks sometimes hesitate to enforce the default rate. However, we always require the bank to formally default the borrower before we close on the note purchase.

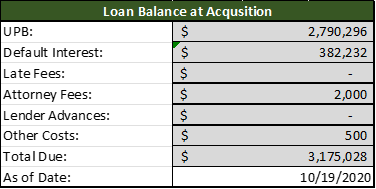

So what is the significance of the default? The borrower was previously only being charged the note interest rate of 4%, equating to ~$310 of per diem (daily) interest. Once 25% is applied, the per diem interest increases to ~$1,911. It puts significant pressure on the borrower to pay off the loan. Moreover, the forbearance agreement allowed us to retroactively apply the default interest back to the original default date. This is why we agreed to make the bank whole and pay them their entire balance. The initial default was a missed loan payment that occurred ~200 days earlier. 200 days x $1,911 = ~$382,200 of default interest. Therefore, the borrower owed:

The note interest was removed and replaced with the default interest. According to the forbearance agreement, if the borrower failed to resume making loan payments in Q4 2020, default interest would apply from the original default date (April 1, 2020). Therefore, the accrued note interest was removed, and the default interest was run from April 1st to the closing date of October 19th .

Post-Acquisition

So now we own the loan (i.e., we are now the lender), and the borrower owes us approximately $325,000 more than we paid for it. How do we make money? There are generally three ways to generate a return:

Restructure the loan so it performs, then sell it or hold it until maturity.

The borrower pays the loan off via a refinance or property sale.

Foreclose and take ownership of the collateral (with the goal of selling it at some point).

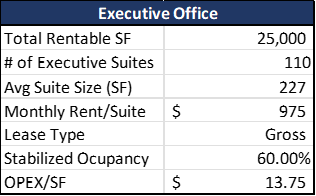

Before diving into each scenario, let’s return to the property itself. At the end of the day, you need to understand the property’s value. This analysis is always completed before acquiring the loan. While the bank typically provides the appraisal from loan origination, it is often too old for valuation purposes. However, it does provide great information. The appraisal was from 2017 on this deal, so the rent roll and financial information were no longer relevant. Yet, it provided us with a general floor plan of the building to identify the number of executive suites and their total rentable square footage. Note, most loan documents require the borrower to report quarterly and/or annually to the lender. A rent roll, operating statement, and tax return are typically required. Some lenders are much better than others at actually collecting the information. You should always request it as part of your due diligence.

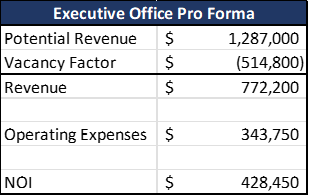

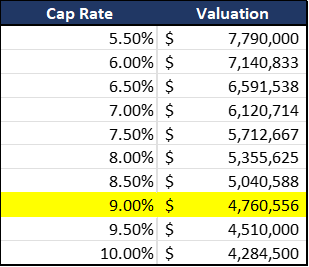

Remember, we are dealing with imperfect information, so we are forced to make assumptions about both rents and expenses. Knowing local sales and leasing brokers is very helpful as they can assist with providing local market conditions. Of course, CoStar and Crexi are good resources, but nothing beats talking to someone on the ground day in and day out. Finally, always be conservative when estimating the collateral value, especially with cap rates. After completing our research, we felt comfortable with the following assumptions and valuation:

At this point, we like our position. We purchased the loan for approximately $2,850,000. Today’s payoff is roughly $3,175,000, and the collateral is likely worth ~$4,760,000 with conservative underwriting assumptions. As previously mentioned, there are other costs to consider, including property taxes, insurance, legal fees, lease-up and holding costs, etc.

Let’s revisit our options now. In this case, I will start with option three, which seems the most profitable.

Option 3: Foreclose and take ownership of the collateral.

Why wouldn’t we pursue this option? If we foreclose and take ownership, we can turn around and sell it for a substantial profit. Unfortunately, there are many constraints. First, if we think the property is worth at least $4,760,000, the borrower likely thinks it is worth more. The borrower could do a “fire sale” and still walk away with over $1,000,000. The collateral was located in a judicial foreclosure state. This is a topic for another day, but know that judicial foreclosures can take a significant amount of time. We are not getting the property back tomorrow.

Second, even if we get a final judgment and the property goes to auction, buyers will likely be ready to bid on it. Remember, we are using a conservative valuation. The valuation is higher if you assume higher rents, lower vacancy, lower OPEX, or a lower cap rate. It could be significantly higher. I haven’t even mentioned legal fees, litigation timeline, the threat of bankruptcy, etc. Big picture, the more perceived equity in the property, the more unlikely it is that you will be able to take possession via a foreclosure.

Option 1: Restructure the loan so it performs, then sell it or hold it until maturity.

Restructuring can take many forms. We could enter another forbearance agreement under favorable terms and conditions. We could offer to change the loan terms to help the borrower resume making payments by lowering the note rate, increasing the amortization period, or providing an interest-only period. We could even offer to do all 3. Private investors typically can get more creative with their loan structures than banks.

We initially debated offering the borrower another forbearance agreement, even if it meant offering an interest rate of less than 25% (remember, we were earning the default rate). Our concern was that the borrower would find a bridge lender to refinance the loan quickly, given the low LTV. Bridge lenders were offering rates in the 9-12% range. We put a lot of time and effort into acquiring the loan. The last thing we wanted was to be paid off immediately, even if that meant accepting a lower rate. We assumed a bridge lender would offer to refinance the entire amount due (i.e., our total payoff) and charge a 10% interest rate and a 2% origination fee. This would bring the 1-year effective rate to ~12%. Therefore, we could offer the borrower a similar deal. In fact, we could get slightly better terms as the borrower would not have to deal with closing costs and attorney fees.

After our first call with the borrower, it was clear that another forbearance agreement would not be on the table. The borrower was not happy about being defaulted. They were very unhappy about the default interest being applied retroactively.

Option 2: Borrower pays the loan off via a refinance or property sale.

At this point, we knew this was the likely outcome. The borrower was too angry to act rationally. Executing a forbearance agreement with us while exploring a refinance or property sale was in their best interest. The borrower's forbearance agreement with the bank was clear that default interest would apply retroactively. Our legal case was solid.

With sufficient equity in the property, we were in no rush to come to a resolution. We were earning $1,911 in interest per day. Theoretically, default interest could run for two years before the total loan payoff exceeded the property’s value. However, there is no guarantee that you will receive all of it. If a judge perceives you are not acting in good faith, they can reduce the default interest granted on the final judgment. For example, the initial foreclosure complaint against the borrower should be filed within a reasonable time frame. A lender shouldn’t default the borrower and wait months before filing the initial foreclosure complaint. Of course, if a lender is trying to work out a resolution with the borrower during that time, then that is acceptable. It’s all about acting in good faith and documenting your attempts so you can show the court if things go south.

With the borrower unwilling to enter negotiations, it was time to file the initial foreclosure complaint. It is essential to hire an experienced local attorney. The attorney should have experience representing lenders in foreclosure cases and have experience in the county with jurisdiction over the matter. Having an attorney familiar with the judges and how they act/rule is very helpful. This will set the stage for your litigation strategy. Do the judges tend to be more lender or borrower friendly? How have they ruled on similar cases in the past?

After filing the initial foreclosure complaint, it took a few weeks before we heard from the borrower’s attorney. We welcomed the delay in responding to our complaint as another ~$50,000 of default interest had accrued. The borrower’s attorney came in, guns blazing. He indicated they were prepared to fight, and our complaint was “preposterous.” His main argument wasn’t on the merits of the legal case but rather on foreclosing during a global pandemic. He reasoned that the judge would be sympathetic to the borrower and ultimately reduce our total payoff (i.e., limit our default interest). At the same time, his client was working on selling the property. The borrower’s objective was to get a favorable ruling from the judge and then sell the property right before the foreclosure auction. If this strategy worked, the borrower’s net proceeds would be significantly higher.

Unfortunately for the borrower, the judge was not in the sympathy business. He was in the business of enforcing legal documents mutually agreed to and executed by both parties. Ultimately, the judge ruled in our favor, and all our default interest and attorney fees were included in the final judgment. The borrower successfully sold the property before the foreclosure auction, and we were paid off.

Results:

The borrower was forced to pay us approximately $3,380,000. The default interest accrued for ~300 days. Here is the final breakdown:

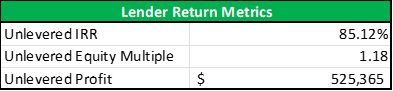

Here are the return metrics for this deal:

While an ~85% IRR is great, we tend to concentrate on a different metric. We were only in the deal for about 100 days, so the IRR looks impressive. We focus on the equity multiple as it better reflects how we grew our wealth. In this case, we received almost 1.2x our initial investment. This was our unlevered return.

Was this a good outcome? Yes, the deal was quite profitable. Was this the ideal outcome? Probably not. We were earning 25% interest on our investment and must reinvest the payoff proceeds. Ideally, we would have been in the deal longer than 100 days, but that is the nature of NPL investing.

Part 2 of this case study will discuss:

modeling the potential returns under the different repayment scenarios

utilizing leverage via a warehouse line

how investor incentives can influence the outcome